What are the best Mercury alternatives, and how do you choose the right business banking platform?

Your business bank account sits at the center of your financial operations. It holds your funds, helps facilitate cash flow, and serves as the platform where you record and manage your financial health. With so many digital banking solutions available today, deciding where to place your company’s money can feel overwhelming.

Since 2017, Mercury has positioned itself as a leading digital neobank, gaining strong visibility in the fintech space. But new competitors have prompted both curious business owners and long-time customers to look for alternatives.

In this guide, we compare the top Mercury alternatives available to businesses today and highlight how Slash’s business banking platform supports modern expense management.¹ Unlike Mercury, Slash offers broad global access and expanded financial tools—including account availability for businesses without a U.S. LLC and native cryptocurrency support for faster, lower-cost international transfers.³, ⁴

Continue reading to learn why Slash stands out as one of the strongest Mercury alternatives available today.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Why consider a Mercury bank alternative?

There are far more digital banking options available today than when Mercury launched in 2017, and many newer platforms now offer capabilities that Mercury lacks. Here are some additional reasons your business may want to explore alternative business banking platforms:

Country restrictions and global payment constraints

Mercury maintains a broad list of restricted countries where its business banking services are limited or unavailable. Founders across much of Africa, as well as in Pakistan, the Philippines, and Ukraine, cannot open a Mercury account. Mercury also charges a 3% foreign transaction fee, compared to Slash’s 1% fee ($0.40 minimum). While both platforms support international SWIFT transfers, Slash's native cryptocurrency support enables access to faster, lower-cost global payments. In other words, Slash is better suited to manage cross-border operations.

Inability to hold or transact cryptocurrency

Mercury does not support crypto or stablecoins and instead limits users to holding and sending traditional fiat currencies. This can be restrictive for businesses that could benefit from blockchain-based payments, which are highly secure, near-instant, and avoid many of the traditional foreign transaction fees. Slash allows companies to hold and pay with USD-pegged stablecoins including USDC and USDT. This flexibility extends to international businesses as well, with Slash’s Global USD account enabling USD payments without a U.S.-registered LLC.

Lack of vertical-specific tools

Mercury promotes itself as an all-in-one banking and expense platform, but the experience is largely uniform regardless of the type of business using it. In contrast, Slash offers banking tools that can be tailored to the needs of different industries, whether that means adjusting card controls for contractor teams or enabling more flexible payment options for businesses operating across borders.

Who are the best competitors to Mercury?

Below are some of our top picks for business banking in 2025, along with breakdowns of the benefits and potential drawbacks of each platform:

Best overall: Slash

Slash is a business banking platform built to give companies greater control, flexibility, and visibility over their finances. Its customizable workflows adapt to a range of industries—from healthcare and e-commerce to marketing and beyond. With real-time insights and detailed analytics, Slash enables teams to make data-driven decisions that support long-term growth. Through an expanded FDIC sweep network, it also provides enhanced coverage for businesses holding larger balances. Additional features include:

- Slash Visa Platinum Card: Earn up to 2% cash back with a corporate charge card that offers real-time spend visibility, customizable controls, unlimited virtual cards, and flexible grouping by team, vendor, or expense category.

- Flexible transfers: Free domestic ACH and wire transfers, global stablecoin payments, support for RTP and FedNow real-time payment rails, and international wires to 180+ countries via SWIFT.

- Integrated accounting: Export your financial data to QuickBooks to streamline invoicing, reconciliation, and expense reporting.

- Stablecoins and Global USD: On- and off-ramps for USDC, USDT, and USDSL for fast, low-cost blockchain payments with no FX fees. Non-U.S. entities can access USD-pegged payments through the Slash Global USD account.

The standard in finance

Slash goes above with better controls, better rewards, and better support for your business.

Best for spend optimization: Brex

Brex is a business banking platform suited for companies that want automated expense management and strong spend controls. It offers corporate cards, accounting integrations, and other finance tools. However, its core focus is still on cards and spend management rather than full-scale banking operations. Eligibility can also be more restrictive, as many features are geared toward venture-backed or larger companies. Additional features include:

- Multi-currency accounts: Localized currency accounts, cross-border card issuance, and VAT tracking.

- Integrated accounting: Ability to export financial data to QuickBooks, Xero, NetSuite, and more.

- Automation tools: Streamlined expense categorization, receipt capture, and real-time spend visibility across teams.

Best for versatile integrations: Rho

Rho is designed for growing small businesses and startups that need more advanced financial infrastructure than a basic online bank platform can offer. The platform emphasizes integrations, connecting with accounting, ERP, HR, and travel tools. While it supports global operations, it does not offer cryptocurrency functionality, and many of its more advanced features are better suited to larger teams. Solo founders or very small businesses may find the platform more complex than they need. Additional features include:

- Banking services: Unified platform offering business checking accounts, savings accounts corporate cards, AP automation, and treasury tools.

- Global operations: Access to multi-currency payments and the SWIFT network for international transfers.

- Advanced workflows: Built-in approval chains and role-based permissions for growing finance teams.

Best for freelancers and small-team ventures: Novo

Novo is a mobile-first business banking platform that may cater to freelancers, solo entrepreneurs, and small businesses that want simple, digital business banking. Novo includes built-in invoicing, budgeting features, and integrations with accounting platforms and payment processors. However, the platform lacks support for advanced features such as global transfers, real-time payments, or multi-user spend controls. Additional features include:

- Invoicing tools: Built-in invoicing to help manage client payments without third-party software. Includes customizable invoice details, automated reminders, and payment tracking.

- Software integrations: Connectivity with Stripe, Shopify, PayPal, QuickBooks, and other SMB tools.

- Simplified savings: Novo’s Reserves feature lets you set savings goals and automatically allocate funds into dedicated savings buckets.

Best for simple access to subaccounts: Relay Financial

Relay Financial is an option for small businesses that want organized cash-flow management through multiple subaccounts. Relay provides a clean interface for managing business checking accounts, debit cards, bill payments, and basic cash-flow tools. Growing companies may find themselves needing more advanced automation or large-scale financial workflows. Relay’s global support is more limited than some competitors, which makes it less suitable for businesses with international teams or cross-border operations. Additional features include:

- Multi-account structure: Up to 20 checking accounts for budgeting, tax planning, or expense buckets.

- Card management: Multiple cards for team members with configurable spending limits. Up to 1.5% cashback on credit card spending.

- Integrations: Connects with tools for accounting and AP management, including QuickBooks, Xero, Plaid, and more.

Best for digital checking accounts: Bluevine

Bluevine is a practical option for small businesses that want a straightforward online checking account with the ability to earn interest on deposits. Its high-yield checking accounts are the biggest draw, while their digital interface can help teams that need simple account management. However, Bluevine’s platform is more limited than full-service fintech solutions. Bluevine doesn’t offer the deeper automation, multi-entity support, or international capabilities that growing businesses may need. Additional features include:

- High-yield checking: Competitive APY on balances, but tied to certain activity requirements.

- Line of credit: Access to working-capital financing for eligible businesses, though approval can be restrictive.

- Simple bill pay: Basic AP functionality for small teams managing vendor payments.

Choosing a business banking alternative to Mercury: key criteria

Choosing the right alternative banking solution for your business depends on a variety of factors: your transaction volumes, team size, software requirements, and more. Still, there are a few qualities to look for in a business banking platform to ensure your company has the tools it needs to grow. Here are the features to look for when evaluating different bank offers:

- Full range of banking services: A more complete product stack reduces the need for multiple vendors and keeps your financial operations centralized. Some platforms can do it all: business checking accounts, savings accounts, high-yield treasury accounts, corporate cards, account software, payment processing, automated expense management tools, and more.

- Integrations: The more integrations your banking platform supports, the more efficiently your business can run. Look for native functionality with widely used tools like QuickBooks, Xero, or Plaid to streamline accounting, reconciliation, invoicing, and account management. Platforms with configurable APIs unlock even more flexibility, allowing you to build custom workflows tailored to your business’s specific needs.

- Customer support reliability: When issues arise—whether it’s a delayed wire, a card decline, or an account freeze—you need a banking partner that can help. Prioritize platforms with reviews that indicate dependable support channels, clear escalation paths, and consistent response times. Slash offers 24/7 support from our team via our website.

- Security and regulatory compliance: Legitimate banking platforms should follow strict security standards, including requirements for KYC, AML, and PCI DSS (if applicable). Features like real-time spend insights, AI-powered monitoring, data encryption and tokenization, or multi-factor authentication can enhance security and keep sensitive financial information safe.

- Scalability and flexibility: Your banking platform should be able to support your business as it grows, not limit it. Look for solutions that can handle higher transaction volumes, support international payments in multiple currencies, and let you add new team members with role-based permissions. Scalable platforms like Slash also offer configurable spend controls, automated approval workflows, and multi-entity support for multiple subsidiaries and payment processors.

- Transparent pricing and fees: Hidden fees and unpredictable charges can erode your margins. Seek providers with transparent pricing models, clearly defined transaction fees, and straightforward subscription structures.

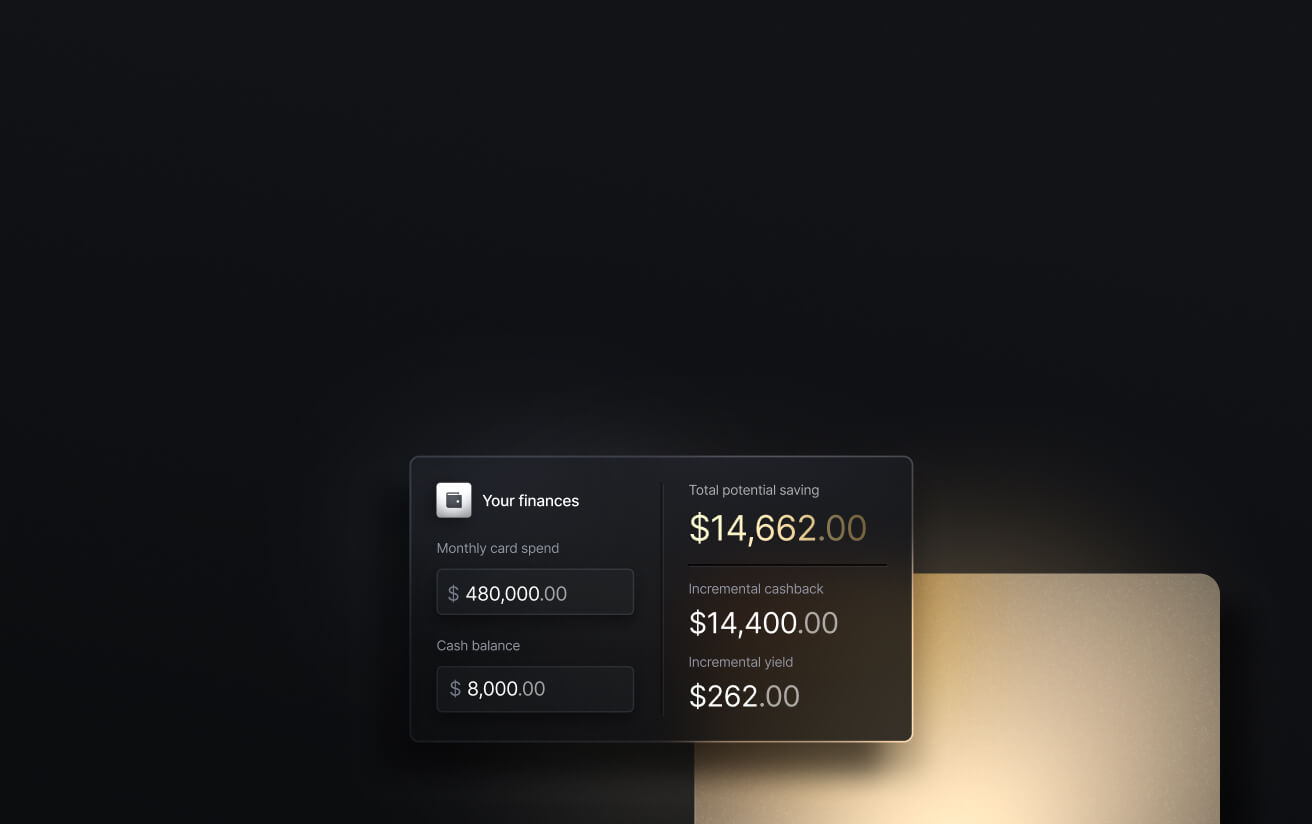

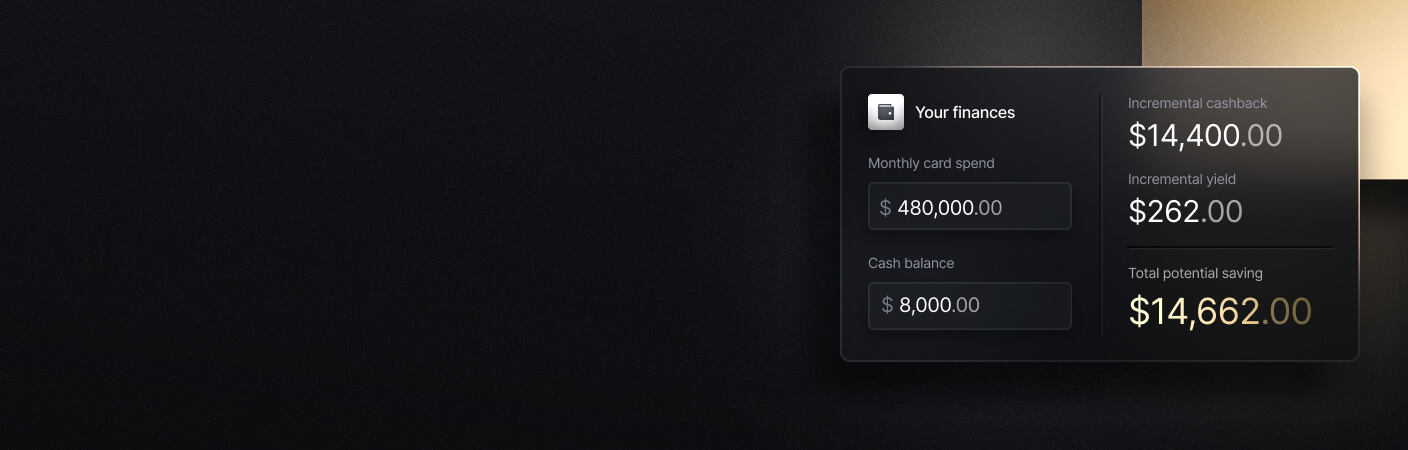

See the ROI behind your spend

Use this calculator to understand impact, then manage and track it all in Slash.

Start optimizing your business banking with Slash

Banking with Mercury can come with trade-offs: limited global support, no access to blockchain-based payments, and high interest rates on credit products.

Slash adapts to the way different industries actually operate. Whether you’re running a construction company, an e-commerce brand, or a healthcare organization, Slash’s customizable workflows can be tailored to your needs.

Slash delivers everything you’d expect from a top-tier business banking platform without the same limitations. Here are some of the features that Mercury can’t match:

- Hold crypto and make payments using on- and off-ramps for USD-pegged stablecoins like USDC, USDT, and USDSL.

- Non-U.S. entities can make USD-based payments through stablecoins using the Slash Global USD account—no U.S. LLC required.

- Send and receive money near-instantly through real-time payment networks like RTP and FedNow.

Apply in less than 10 minutes today

Join the 5,000+ businesses already using Slash.

Frequently asked questions

Can I switch from Mercury to another bank without closing my existing accounts immediately?

Yes. Most banking providers allow you to open a new account without closing your existing one, and it’s often preferable to keep both accounts active temporarily to ensure a smooth transition. Start by opening your new account, then migrate key transactions, and update integrations and automations. Only close your Mercury account once all payments and balances have fully transferred.

Do any Mercury alternatives offer cryptocurrency-friendly banking services?

Mercury does not support crypto-related banking services. While crypto and stablecoin functionality is still not widespread among most neobanks, Slash offers built-in stablecoin on- and off-ramps for USDC, USDT, and USDSL. This allows you to send and receive USD-pegged stablecoin payments directly within the Slash dashboard—a capability most competitors do not yet offer.

Cryptocurrency Conversion Guide: How Crypto On/Off Ramps Transform Business Payments

Are there options for virtual cards with cashback rewards similar to Mercury?

Yes. Several neobanks and fintech platforms offer virtual cards with cashback programs. However, few match the reward structure of the Slash Visa Platinum Card, which earns up to 2% cashback on purchases. Slash’s platform also includes customizable spend controls, card groupings, and unlimited virtual card issuance.

Unlimited Cashback vs. Tiered Rewards: Key Differences Explained

Read more from us